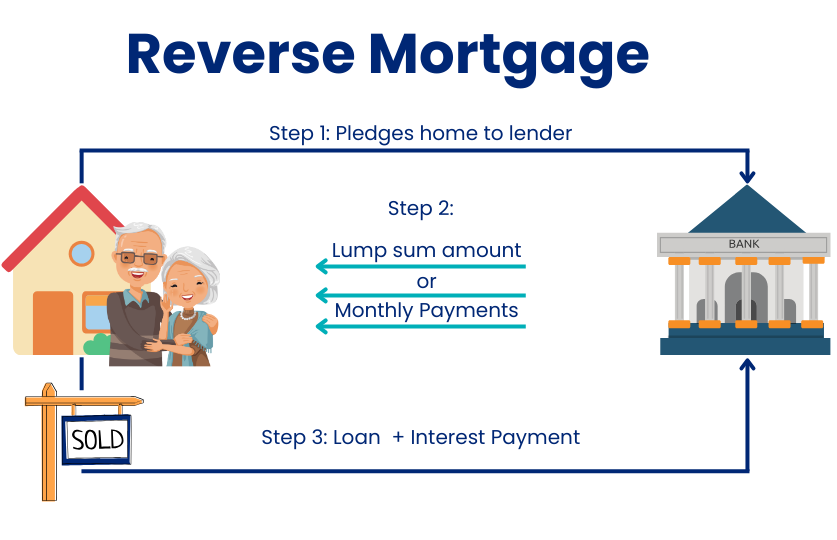

Access to Cash Without Selling Your Home

Access to Cash Without Selling Your Home

For many retirees, their home is their most valuable asset, but selling isn’t always desirable. A reverse mortgage allows them to stay in their home while using some of its equity.

No Mandatory Repayments

Unlike traditional loans, borrowers aren’t required to make repayments. The loan is repaid when the house is sold, easing financial pressure in retirement.

Flexible Access to Funds

Funds can be taken as a lump sum, a regular income, or a line of credit, providing flexibility to suit different financial needs.

Government Protection (No Negative Equity Guarantee)

Australian laws ensure borrowers (or their estates) can’t owe more than the value of the home, even if the loan balance exceeds the sale price.

Maintain Ownership & Control

Borrowers retain ownership of their home and can live in it for as long as they want.

Use the Money However You Like

Common uses include:

- Covering living expenses

- Paying for home renovations or modifications

- Funding medical or aged care costs

- Gifting money to children (e.g., helping them buy a home)

- Paying off existing debts

Interest Compounds Over Time

Interest Compounds Over Time

Unlike traditional loans where interest reduces as you make payments, a reverse mortgage’s interest compounds, meaning the debt grows quickly over time.

Reduces Your Estate’s Value

The loan and interest must be repaid when the property is sold, leaving less for beneficiaries.

Impact on Pension & Government Benefits

Receiving a lump sum or regular payments from a reverse mortgage can affect eligibility for the Age Pension and other government benefits.

Costs & Fees

Borrowers may face:

- Establishment fees

- Ongoing service fees

- Valuation and legal fees

- Discharge costs when repaying the loan

Possible Need to Sell Sooner Than Planned

If the loan grows too large, selling the home earlier than expected may become necessary to clear the debt.